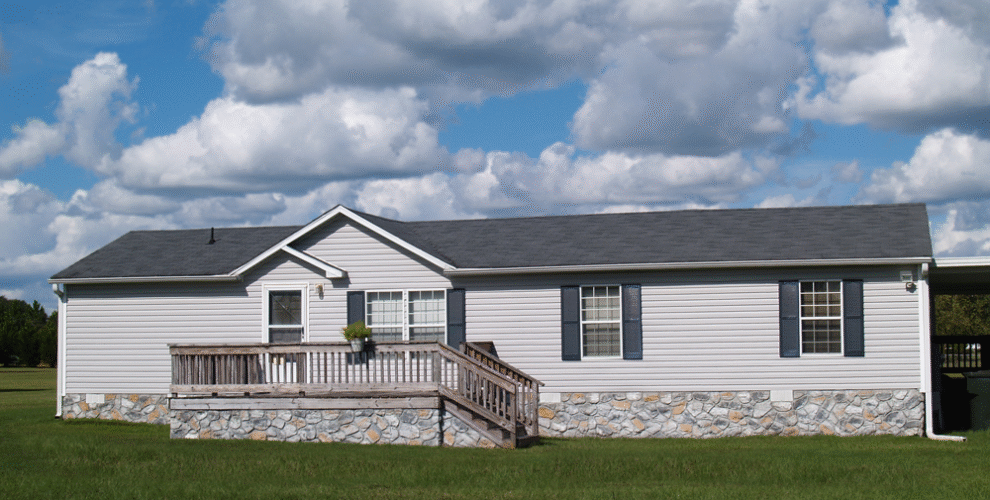

The nation’s lack of affordable housing options has buyers searching for practical, economic alternative to stick-built housing. One increasingly attractive alternative is manufactured housing. Manufactured housing has come a long way since the mobile home parks of the past. The cookie-cutter, one-story “trailers” that once had a negative reputation are giving way to higher-end, manufactured homes that are nearly indistinguishable from their foundation-built peers.

In this article, we look at the growth of the manufactured housing industry, its current demand drivers, and why the sector is drawing the attention of individual owner-occupants and institutional investors alike.

What is manufactured housing?

Manufactured housing is a subset of the residential housing sector. Manufactured homes are units that have been primarily or entirely constructed in climate-controlled off-site facilities. Units can be assembled either on- or off-site, with the latter requiring flatbed transportation of the home to its final destination. Most manufactured homes are built on top of concrete slabs or wheeled platforms instead of built into more permanent foundations. As such, manufactured housing must be strapped or otherwise anchored to the ground.

The off-site, assembly line-like construction process generally leads to efficiencies that lower the cost of construction. These cost savings can be passed on to the end users, thereby making manufactured homes a more affordable alternative when compared to traditional residential properties.

Modular homes are a specific type of manufactured housing. Modular construction essentially employs a “kit of parts” approach in which various building categories (e.g., kitchens, bathrooms, bedrooms) are constructed using lean processes and then each of these modules is combined with the others, depending on the home builder or buyer’s parameters, and then shipped to the destination to be assembled on-site.

Unlike traditional mobile homes, manufactured housing can come in all shapes and sizes. Homes can be as small as 500 square feet or as large as 3,000 square feet or more. They can be made with many materials, amenities and finishes and depending on the specifics, can take just days or weeks to make. Other projects can take months to complete self-storage real estate investment.

A Brief History of Manufactured Housing

Manufactured housing has come a long way over the past 50 years, particularly as technology has improved and allowed for more streamlined factory construction processes. Manufactured housing was once thought to be of lower quality than traditional, stick-built homes. Today, the quality of manufactured housing is often on par with the quality of other entry-level homes.

Moreover, in the 1970s and 1980s, most manufactured homes were located in land-lease communities. A homeowner would “lease” the land from an owner/operator and would then utilize a personal property loan to acquire the home that was sited on that plot of land. Today, more than half of manufactured homes are sold to buyers who place the property on privately-owned sites, including more traditional residential subdivisions.

There are a few reasons for this shift: first, contemporary manufactured homes are often larger and more attractive than those that were built in the decades prior. Therefore, these homes seamlessly blend into newer and more established residential communities. Many people will buy a plot of land and rather than waiting to construct a new home, will simply have their dream home delivered – a process that can save significant time and money. Second, as the options for manufactured housing have expanded, this is a product type that has grown in favor among buyers of all types. Manufactured homes (or “mobile homes”) are no longer considered to be housing for low-income renters or buyers.

Demand Drivers for Manufactured Housing

Manufactured housing is experiencing a renaissance. There are several reasons why this niche product type is starting to attract attention from buyers – individual and institutional alike.

- Improved Product Quality: Today’s manufactured housing is built in climate-controlled factories with strict quality assurance and supervision of each step of the process. This has improved product quality, particularly around energy efficiency and durability. Materials, amenities, and finishes are now more robust (e.g., granite countertops, central AC, high-end appliances) and can be integrated into manufactured homes, large and small. The improved product quality has made manufactured homes often indistinguishable from their stick-built peers.

- Easing of Regulatory Barriers: For many years, pervasive and ongoing opposition to manufactured homes prevented manufactured housing communities from being developed. As product quality has improved, opposition to manufactured homes has declined and made it more feasible for people to invest in or purchase manufactured housing for their personal use and enjoyment.

- Lack of Entry-Level Housing: Amid the nation’s affordable housing crisis, manufactured housing presents a viable entry-level housing alternative – particularly in coastal communities, such as Florida, where workforce housing is increasingly hard to come by. Manufactured homes cost approximately half the cost, per square foot, to construct relative to traditional stick-built homes. This makes manufactured housing an attractive option for entry-level buyers and cost-conscious renters alike.

- Broad Appeal: First-time homebuyers are not the only demographic drawn to manufactured housing. Baby Boomers, particularly those looking to downsize or retire in warmer climates, are driving demand for manufactured homes.

- Low Vacancy Rates: Given the lack of affordable housing options, and given the growing appeal of manufactured housing, the vacancy rate of existing manufactured home communities has plummeted. According to a recent Marcus & Millichap study, the vacancy rate at manufactured housing communities in coastal areas like Miami, San Jose, Denver, and Salt Lake City hovered at or below 1 percent last year.

- Increasing Rents: With limited inventory, land-lease manufactured housing operators have been able to increase rents. According to a recent survey, 93 percent of operators indicated steady or rising rents in 2020. The Northeast led rent growth with a 4.6 percent gain, followed by the Gulf Coast and Mountain Region which both registered a 4.5 percent year-over-year increase. Lot rent in coastal communities is beginning to edge close to $1,000 per month in some markets.

Manufactured Housing as an Investment

Given the demand drivers discussed above, it should be no surprise that investors are starting to consider adding manufactured housing communities to their portfolios. This is especially true as management of these developments has improved. Until recently, most manufactured housing communities were locally owned and operated, often by inexperienced mom and pop investors. Today, more professional investors, like DST sponsor companies, are acquiring these communities and introducing professional management. In doing so, they are in a better position to work to increase rents and by extension, increase property values – value that, if achieved, can then be passed on to investors.

As the value of manufactured housing communities becomes more apparent, larger investors are entering the fray. In 1994, four new REITs formed – the first designed to specifically invest in this product type (Manufactured Home Communities, ROC Communities, SUN Communities, and Chateau Properties). These REITs continue to outperform many of their more traditional residential REIT peers. Today, several other REITs have expanded their portfolios to include manufactured housing.

Manufactured housing is also increasingly seen as a stable investment. Land-lease communities generally have low turnover and stable (and increasing) rents. By some estimates, the national occupancy rates of land-leased manufactured home communities hovers above 90 percent.

The Outlook for Manufactured Housing

The outlook for manufactured housing remains strong – perhaps, stronger than ever. The nation’s lack of economic living options may only further the appeal of manufactured housing.

From an investment perspective, people should be prepared to see yields compress. As more institutional capital has entered the fray, most of the high-quality manufactured home communities have already been purchased. Cap rates are already beginning to come down. In turn, many investors are now buying smaller, less well-located communities with expansion and/or value-add strategies in mind.

Manufactured housing looks nearly nothing like it did just a few decades ago. The manufactured homes being constructed today are high-end yet affordable. They appeal to individual buyers, renters, and investors of all scale. That said, despite the sector’s growing popularity, there is still significant opportunity – particularly in an era where other residential product types continue to climb. People will always need somewhere to live, and absent more affordable options, manufactured homes may present an attractive option for the masses.

Perch Wealth works with large, experienced, and professional DST sponsor companies that offer manufactured housing investment opportunities to accredited investors looking to invest their 1031 exchange funds. Contact Perch Wealth today to find out more about this asset class and investment opportunities.